Because I have talked about differentiation ad nauseum, I’m always looking for ways to see how identity/biometric and technology vendors have differentiated themselves. Yes, almost all of them overuse the word “trust,” but there is still some differentiation out there.

And I found a source that measured differentiation (or “unique positioning”) in various market segments. Using this source, I chose to concentrate on vendors who concentrate on identity verification (or “identity proofing & verification,” but close enough).

Before you read this, I want to caution you that this is NOT a thorough evaluation of The Prism Project deepfake and synthetic identity report. After some preliminaries, it focuses on one small portion of the report, concentrating on ONLY one “beam” (IDV) and ONLY one evaluation factor (differentiation).

Four facts about the report

First, the report is comprehensive. It’s not merely a list of ranked vendors, but also provides a, um, deep dive into deepfakes and synthetic identity. Even if you don’t care about the industry players, I encourage you to (a) download the report, and (b) read the 8 page section entitled “Crash Course: The Identity Arms Race.”

The crash course starts by describing digital identity and the role that biometrics plays in digital identity. It explains how banks, government agencies, and others perform identity verification; we’ll return to this later.

Then it moves on to the bad people who try to use “counterfeit identity elements” in place of “authentic identity elements.” The report discusses spoofs, presentation attacks, countermeasures such as multi-factor authentication, and…

Well, just download the report and read it yourself. If you want to understand deepfakes and synthetic identities, the “Crash Course” section will educate you quickly and thoroughly, as will the remainder of the report.

Synthetic Identity Fraud Attacks. Copyright 2025 The Prism Project.

Second, the report is comprehensive. Yeah, I just said that, but it’s also comprehensive in the number of organizations that it covers.

In a previous life I led a team that conducted competitive analysis on over 80 identity organizations.

I then subsequently encountered others who estimated that there are over 100 organizations.

This report evaluates over 200 organizations. In part this is because it includes evaluations of “relying parties” that are part of the ecosystem. (Examples include Mastercard, PayPal, and the Royal Bank of Canada who obviously don’t want to do business with deepfakes or synthetic identities.) Still, the report is amazing in its organizational coverage.

Third, the report is comprehensive. In a non-lunatic way, the report categorizes each organization into one or more “beams”:

The aforementioned relying parties

Core identity technology

Identity platforms

Integrators & solution providers

Passwordless authentication

Environmental risk signals

Infrastructure, community, culture

And last but first (for purposes of this post), identity proofing and verification.

Fourth, the report is comprehensive. Yes I’m repetitive, but each of the 200+ organizations are evaluated on a 0-6 scale based upon seven factors. In listed order, they are:

Growth & Resources

Market Presence

Proof Points

Unique Positioning, defined as “Unique Value Proposition (UVP) along with diferentiable technology and market innovation generally and within market sector.”

Business Model & Strategy

Biometrics and Document Authentication

Deepfakes & Synthetic Identity Leadership

In essence, the wealth of data makes this report look like a NIST report: there are so many individual “slices” of the prism that every one of the 200+ organizations can make a claim about how it was recognized by The Prism Project. And you’ve probably already seen some organizations make such claims, just like they do whenever a new NIST report comes out.

So let’s look at the tiny slice of the prism that is my, um, focus for this post.

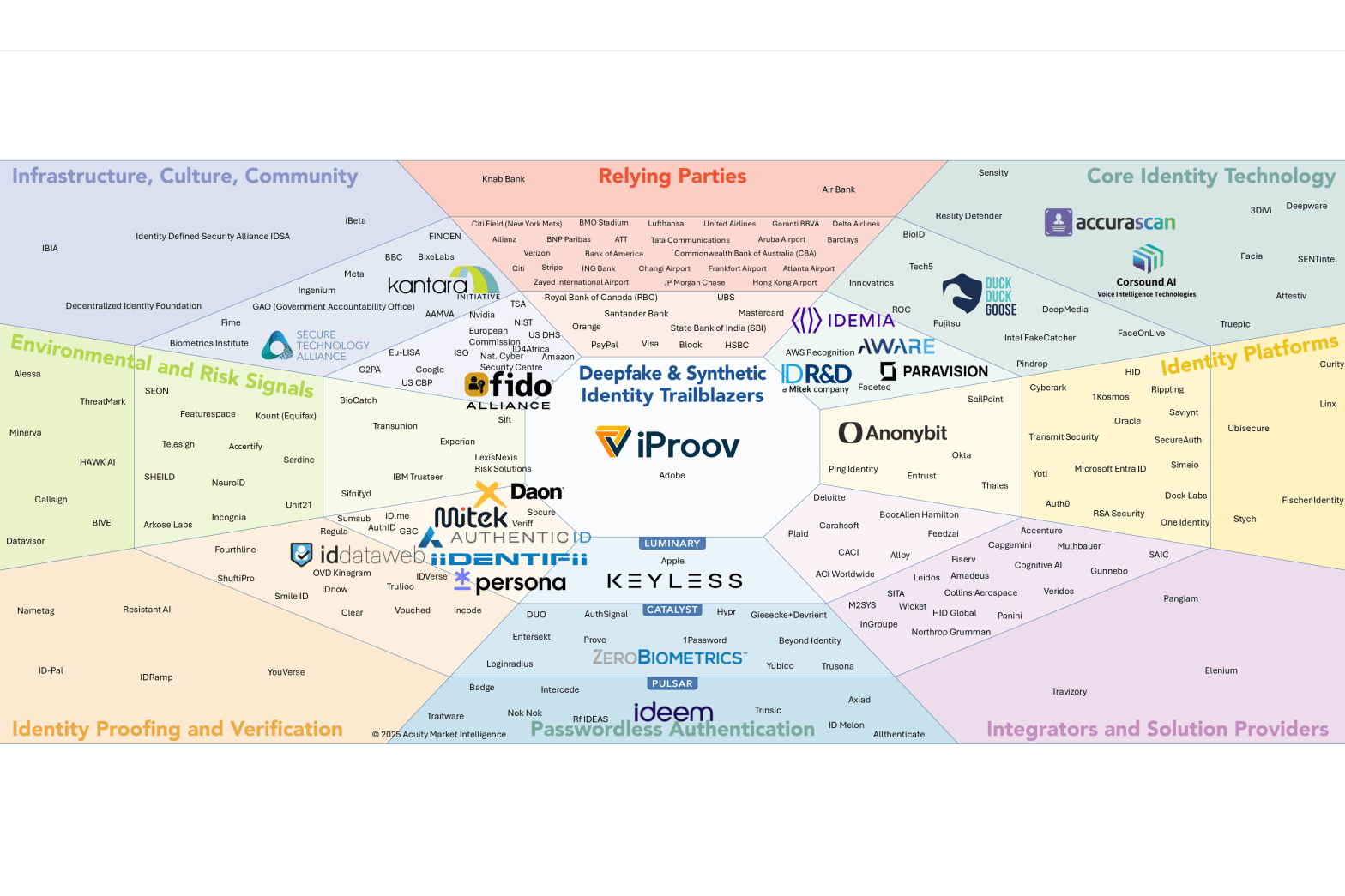

Unique positioning in the IDV slice of the Prism

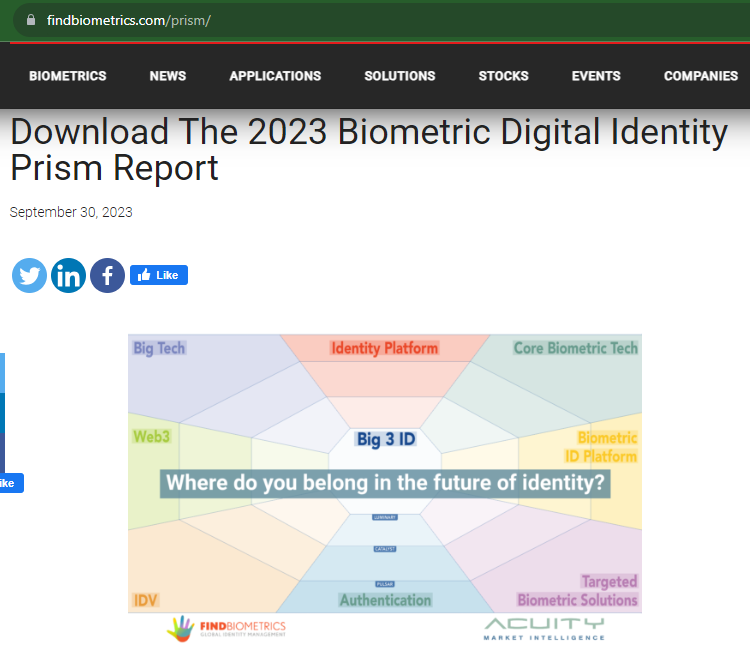

So, here’s the moment all of you have been waiting for. Which organizations are in the Biometric Digital Identity Deepfake and Synthetic Identity Prism?

Deepfake and Synthetic Identity Prism. Copyright 2025 The Prism Project.

Yeah, the text is small. Told you there were a lot of organizations.

For my purposes I’m going to concentrate on the “identity proofing and verification” beam in the lower left corner. But I’m going to dig deeper.

In the illustration above, organizations are nearer or farther from the center based upon their AVERAGE score for all 7 factors I listed previously. But because I want to concentrate on differentiation, I’m only going to look at the identity proofing and verification organizations with high scores (between 5 and the maximum of 6) for the “unique positioning” factor.

I’ll admit my methodology is somewhat arbitrary.

There’s probably no great, um, difference between an organization with a score of 4.9 and one with a score of 5. But you can safely state that an organization with a “unique positioning” score of 2 isn’t as differentiated from one with a score of 5.

And this may not matter. For example, iBeta (in the infrastructure – culture – community beam) has a unique positioning score of 2, because a lot of organizations do what iBeta does. But at the same time iBeta has a biometric commitment of 4.5. They don’t evaluate refrigerators.

So, here’s my list of identity proofing and verification organizations who scored between 5 and 6 for the unique positioning factor:

ID.me

iiDENTIFii

Socure

Using the report as my source, these three identity verification companies have offerings that differentiate themselves from others in the pack.

Although I’m sure the other identity verification vendors can be, um, trusted.

But perhaps you would prefer to hear from someone who knows what they’re talking about.

On a webcast this morning, C. Maxine Most of The Prism Project reminded us that the “Biometric Digital Identity Deepfake and Synthetic Identity Prism Report” is scheduled for publication in May 2025, just a little over a month from now.

As with all other Prism Project publications, I expect a report that details the identity industry’s solutions to battle deepfakes and synthetic identities, and the vendors who provide them.

And the report is coming from one of the few industry researchers who knows the industry. Max doesn’t write synthetic identity reports one week and refrigerator reports the next, if you know what I mean.

At this point The Prism Project is soliciting sponsorships. Quality work doesn’t come for free, you know. If your company is interested in sponsoring the report, visit this link.

While waiting for Max, here are the Five Tops

And while you’re waiting for Max’s authoritative report on deepfakes and synthetic identity, you may want to take a look at Min’s (my) views, such as they are. Here are my current “five tops” posts on deepfakes and synthetic identity.

The Prism Project’s home page at https://www.the-prism-project.com/, illustrating the Biometric Digital Identity Prism as of March 2024. From Acuity Market Intelligence and FindBiometrics.

With over 100 firms in the biometric industry, their offerings are going to naturally differ—even if all the firms are TRYING to copy each other and offer “me too” solutions.

I’ve worked for over a dozen biometric firms as an employee or independent contractor, and I’ve analyzed over 80 biometric firms in competitive intelligence exercises, so I’m well aware of the vast implementation differences between the biometric offerings.

Some of the implementation differences provoke vehement disagreements between biometric firms regarding which choice is correct. Yes, we FIGHT.

Let’s look at three (out of many) of these implementation differences and see how they affect YOUR company’s content marketing efforts—whether you’re engaging in identity blog post writing, or some other content marketing activity.

The three biometric implementation choices

Firms that develop biometric solutions make (or should make) the following choices when implementing their solutions.

Presentation attack detection. Assuming the solution incorporates presentation attack detection (liveness detection), or a way of detecting whether the presented biometric is real or a spoof, the firm must decide whether to use active or passive liveness detection.

Age assurance. When choosing age assurance solutions that determine whether a person is old enough to access a product or service, the firm must decide whether or not age estimation is acceptable.

Biometric modality. Finally, the firm must choose which biometric modalities to support. While there are a number of modality wars involving all the biometric modalities, this post is going to limit itself to the question of whether or not voice biometrics are acceptable.

I will address each of these questions in turn, highlighting the pros and cons of each implementation choice. After that, we’ll see how this affects your firm’s content marketing.

(I)nstead of capturing a true biometric from a person, the biometric sensor is fooled into capturing a fake biometric: an artificial finger, a face with a mask on it, or a face on a video screen (rather than a face of a live person).

This tomfoolery is called a “presentation attack” (becuase you’re attacking security with a fake presentation).

And an organization called iBeta is one of the testing facilities authorized to test in accordance with the standard and to determine whether a biometric reader can detect the “liveness” of a biometric sample.

(Friends, I’m not going to get into passive liveness and active liveness. That’s best saved for another day.)

Now I could cite a firm using active liveness detection to say why it’s great, or I could cite a firm using passive liveness detection to say why it’s great. But perhaps the most balanced assessment comes from facia, which offers both types of liveness detection. How does facia define the two types of liveness detection?

Active liveness detection, as the name suggests, requires some sort of activity from the user. If a system is unable to detect liveness, it will ask the user to perform some specific actions such as nodding, blinking or any other facial movement. This allows the system to detect natural movements and separate it from a system trying to mimic a human being….

Passive liveness detection operates discreetly in the background, requiring no explicit action from the user. The system’s artificial intelligence continuously analyses facial movements, depth, texture, and other biometric indicators to detect an individual’s liveness.

Pros and cons

Briefly, the pros and cons of the two methods are as follows:

While active liveness detection offers robust protection, requires clear consent, and acts as a deterrent, it is hard to use, complex, and slow.

Passive liveness detection offers an enhanced user experience via ease of use and speed and is easier to integrate with other solutions, but it incorporates privacy concerns (passive liveness detection can be implemented without the user’s knowledge) and may not be used in high-risk situations.

So in truth the choice is up to each firm. I’ve worked with firms that used both liveness detection methods, and while I’ve spent most of my time with passive implementations, the active ones can work also.

A perfect wishy-washy statement that will get BOTH sides angry at me. (Except perhaps for companies like facia that use both.)

If you need to know a person’s age, you can ask them. Because people never lie.

Well, maybe they do. There are two better age assurance methods:

Age verification, where you obtain a person’s government-issued identity document with a confirmed birthdate, confirm that the identity document truly belongs to the person, and then simply check the date of birth on the identity document and determine whether the person is old enough to access the product or service.

Age estimation, where you don’t use a government-issued identity document and instead examine the face and estimate the person’s age.

I changed my mind on age estimation

I’ve gone back and forth on this. As I previously mentioned, my employment history includes time with a firm produces driver’s licenses for the majority of U.S. states. And back when that firm was providing my paycheck, I was financially incentivized to champion age verification based upon the driver’s licenses that my company (or occasionally some inferior company) produced.

But as age assurance applications moved into other areas such as social media use, a problem occurred since 13 year olds usually don’t have government IDs. A few of them may have passports or other government IDs, but none of them have driver’s licenses.

But does age estimation work? I’m not sure if ANYONE has posted a non-biased view, so I’ll try to do so myself.

The pros of age estimation include its applicability to all ages including young people, its protection of privacy since it requires no information about the individual identity, and its ease of use since you don’t have to dig for your physical driver’s license or your mobile driver’s license—your face is already there.

The huge con of age estimation is that it is by definition an estimate. If I show a bartender my driver’s license before buying a beer, they will know whether I am 20 years and 364 days old and ineligible to purchase alcohol, or whether I am 21 years and 0 days old and eligible. Estimates aren’t that precise.

Fingerprints, palm prints, faces, irises, and everything up to gait. (And behavioral biometrics.) There are a lot of biometric modalities out there, and one that has been around for years is the voice biometric.

I’ve discussed this topic before, and the partial title of the post (“We’ll Survive Voice Spoofing”) gives away how I feel about the matter, but I’ll present both sides of the issue.

No one can deny that voice spoofing exists and is effective, but many of the examples cited by the popular press are cases in which a HUMAN (rather than an ALGORITHM) was fooled by a deepfake voice. But voice recognition software can also be fooled.

Take a study from the University of Waterloo, summarized here, that proclaims: “Computer scientists at the University of Waterloo have discovered a method of attack that can successfully bypass voice authentication security systems with up to a 99% success rate after only six tries.”

If you re-read that sentence, you will notice that it includes the words “up to.” Those words are significant if you actually read the article.

In a recent test against Amazon Connect’s voice authentication system, they achieved a 10 per cent success rate in one four-second attack, with this rate rising to over 40 per cent in less than thirty seconds. With some of the less sophisticated voice authentication systems they targeted, they achieved a 99 per cent success rate after six attempts.

Other voice spoofing studies

Similar to Gender Shades, the University of Waterloo study does not appear to have tested hundreds of voice recognition algorithms. But there are other studies.

The 2021 NIST Speaker Recognition Evaluation (PDF here) tested results from 15 teams, but this test was not specific to spoofing.

A test that was specific to spoofing was the ASVspoof 2021 test with 54 team participants, but the ASVspoof 2021 results are only accessible in abstract form, with no detailed results.

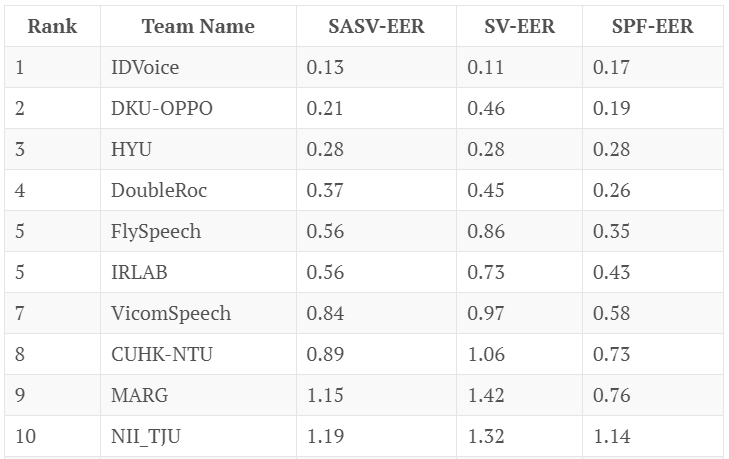

Another test, this one with results, is the SASV2022 challenge, with 23 valid submissions. Here are the top 10 performers and their error rates.

You’ll note that the top performers don’t have error rates anywhere near the University of Waterloo’s 99 percent.

So some firms will argue that voice recognition can be spoofed and thus cannot be trusted, while other firms will argue that the best voice recognition algorithms are rarely fooled.

What does this mean for your company?

Obviously, different firms are going to respond to the three questions above in different ways.

For example, a firm that offers face biometrics but not voice biometrics will convey how voice is not a secure modality due to the ease of spoofing. “Do you want to lose tens of millions of dollars?”

A firm that offers voice biometrics but not face biometrics will emphasize its spoof detection capabilities (and cast shade on face spoofing). “We tested our algorithm against that voice fake that was in the news, and we detected the voice as a deepfake!”

There is no universal truth here, and the message your firm conveys depends upon your firm’s unique characteristics.

And those characteristics can change.

Once when I was working for a client, this firm had made a particular choice with one of these three questions. Therefore, when I was writing for the client, I wrote in a way that argued the client’s position.

After I stopped working for this particular client, the client’s position changed and the firm adopted the opposite view of the question.

Therefore I had to message the client and say, “Hey, remember that piece I wrote for you that said this? Well, you’d better edit it, now that you’ve changed your mind on the question…”

Bear this in mind as you create your blog, white paper, case study, or other identity/biometric content, or have someone like the biometric content marketing expert Bredemarket work with you to create your content. There are people who sincerely hold the opposite belief of your firm…but your firm needs to argue that those people are, um, misinformed.

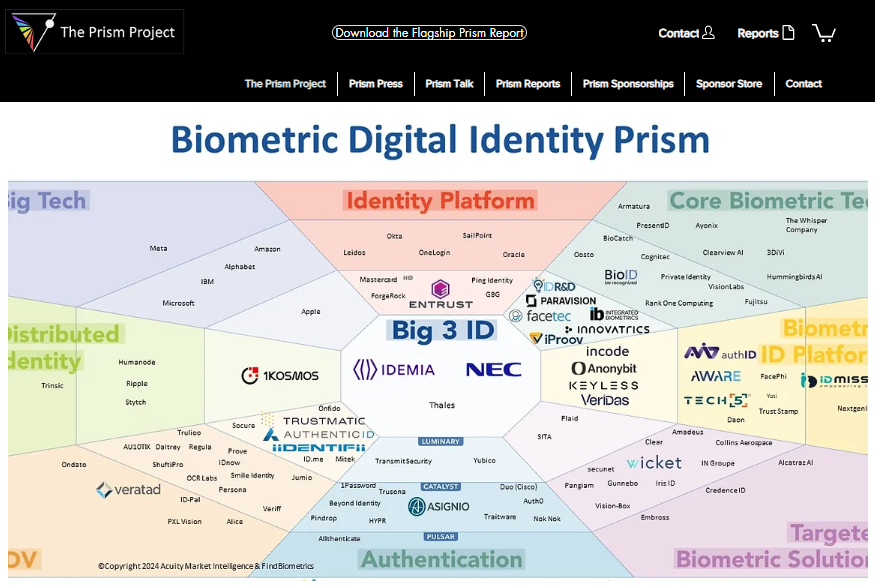

For those who don’t know, the Prism presents an organized view of all of the digital identity companies—or at least the ones that FindBiometrics and Acuity Market Intelligence knew about. In the last few days, they were literally beggin’ to give companies a last chance for inclusion.

On Monday, I began to see a trickle of companies that talked about their place on the Prism, including iProov and Trustmatic.

On September 30, FindBiometrics and Acuity Market Intelligence released the production version of the Biometric Digital Identity Prism Report. You can request to download it here.

But FindBiometrics and Acuity Market Intelligence didn’t invent the Big 3. The concept has been around for 40 years. And two of today’s Big 3 weren’t in the Big 3 when things started. Oh, and there weren’t always 3; sometimes there were 4, and some could argue that there were 5.

So how did we get from the Big 3 of 40 years ago to the Big 3 of today?

The Big 3 in the 1980s

Back in 1986 (eight years before I learned how to spell AFIS) the American National Standards Institute, in conjunction with the National Bureau of Standards, issued ANSI/NBS-ICST 1-1986, a data format for information interchange of fingerprints. The PDF of this long-superseded standard is available here.

When creating this standard, ANSI and the NBS worked with a number of law enforcement agencies, as well as companies in the nascent fingerprint industry. There is a whole list of companies cited at the beginning of the standard, but I’d like to name four of them.

De La Rue Printrak, Inc.

Identix, Inc.

Morpho Systems

NEC Information Systems, Inc.

While all four of these companies produced computerized fingerprinting equipment, three of them had successfully produced automated fingerprint identification systems, or AFIS. As Chapter 6 of the Fingerprint Sourcebook subsequently noted:

Morpho Systems resulted from French AFIS efforts, separate from those of the FBI. These efforts launched Morpho’s long-standing relationship with the French National Police, as well as a similar relationship (now former relationship) with Pierce County, Washington.

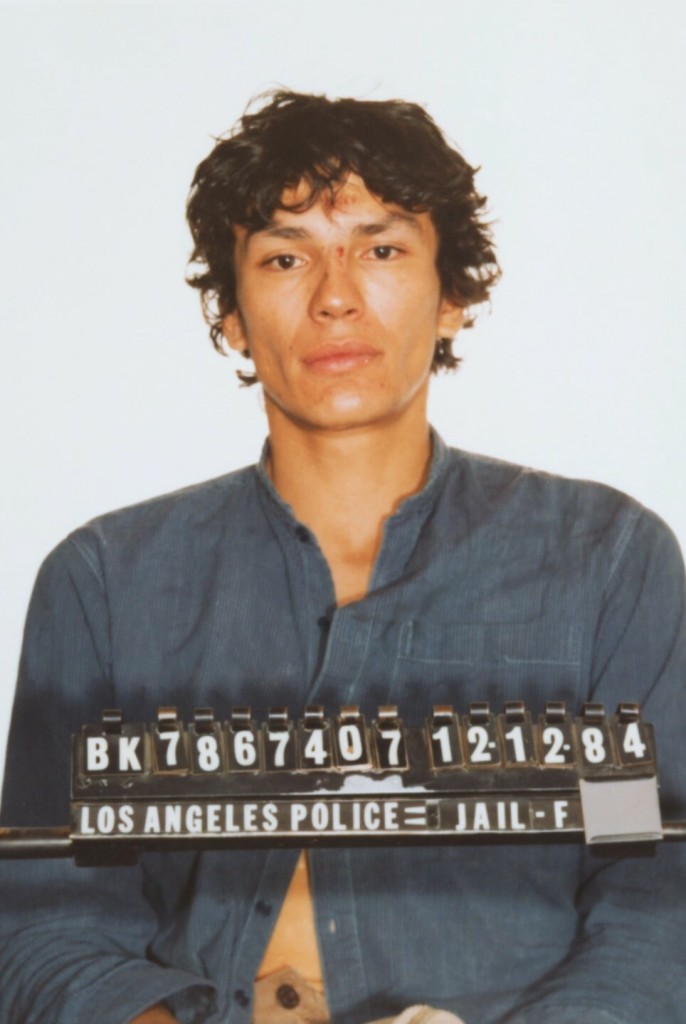

NEC had deployed AFIS equipment for the National Police Academy of Japan, and (after some prodding; read Chapter 6 for the story) the city of San Francisco. Eventually the state of California obtained an NEC system, which played a part in the identification of “Night Stalker” Richard Ramirez.

After the success of the San Francisco and California AFIS systems, many other jurisdictions began clamoring for AFIS of their own, and turned to these three vendors to supply them.

The Big 4 in the 1990s

But in 1990, these three firms were joined by a fourth upstart, Cogent Systems of South Pasadena, California.

While customers initially preferred the Big 3 to the upstart, Cogent Systems eventually installed a statewide system in Ohio and a border control system for the U.S. government, plus a vast number of local systems at the county and city level.

Between 1991 and 1994, the (Immigfation and Naturalization Service) conducted several studies of automated fingerprint systems, primarily in the San Diego, California, Border Patrol Sector. These studies demonstrated to the INS the feasibility of using a biometric fingerprint identification system to identify apprehended aliens on a large scale. In September 1994, Congress provided almost $30 million for the INS to deploy its fingerprint identification system. In October 1994, the INS began using the system, called IDENT, first in the San Diego Border Patrol Sector and then throughout the rest of the Southwest Border.

I was a proposal writer for Printrak (divested by De La Rue) in the 1990s, and competed against Cogent, Morpho, and NEC in AFIS procurements. By the time I moved from proposals to product management, the next redefinition of the “big” vendors occurred.

The Big 3 in 2003

There are a lot of name changes that affected AFIS participants, one of which was the 1988 name change of the National Bureau of Standards to the National Institute of Standards and Technology (NIST). As fingerprints and other biometric modalities were increasingly employed by government agencies, NIST began conducting tests of biometric systems. These tests continue to this day, as I have previously noted.

One of NIST’s first tests was the Fingerprint Vendor Technology Evaluation of 2003 (FpVTE 2003).

For those who are familiar with NIST testing, it’s no surprise that the test was thorough:

FpVTE 2003 consists of multiple tests performed with combinations of fingers (e.g., single fingers, two index fingers, four to ten fingers) and different types and qualities of operational fingerprints (e.g., flat livescan images from visa applicants, multi-finger slap livescan images from present-day booking or background check systems, or rolled and flat inked fingerprints from legacy criminal databases).

Eighteen vendors submitted their fingerprint algorithms to NIST for one or more of the various tests, including Bioscrypt, Cogent Systems, Identix, SAGEM MORPHO (SAGEM had acquired Morpho Systems), NEC, and Motorola (which had acquired Printrak). And at the conclusion of the testing, the FpVTE 2003 summary (PDF) made this statement:

Of the systems tested, NEC, SAGEM, and Cogent produced the most accurate results.

Which would have been great news if I were a product manager at NEC, SAGEM, and Cogent.

Unfortunately, I was a product manager at Motorola.

The effect of this report was…not good, and at least partially (but not fully) contributed to Motorola’s loss of its long-standing client, the Royal Canadian Mounted Police, to Cogent.

The Big 3, 4, or 5 after 2003

So what happened in the years after FpVTE was released? Opinions vary, but here are three possible explanations for what happened next.

Did the Big 3 become the Big 4 again?

Now I probably have a bit of bias in this area since I was a Motorola employee, but I maintain that Motorola overcame this temporary setback and vaulted back into the Big 4 within a couple of years. Among other things, Motorola deployed a national 1000 pixels-per-inch (PPI) system in Sweden several years before the FBI did.

Did the Big 3 remain the Big 3?

Motorola’s arch-enemies at Sagem Morpho had a different opinion, which was revealed when the state of West Virginia finally got around to deploying its own AFIS. A bit ironic, since the national FBI AFIS system IAFIS was located in West Virginia, or perhaps not.

Anyway, Motorola had a very effective sales staff, as was apparent when the state issued its Request for Proposal (RFP) and explicitly said that the state wanted a Motorola AFIS.

That didn’t stop Cogent, Identix, NEC, and Sagem Morpho from bidding on the project.

After the award, Dorothy Bullard and I requested copies of all of the proposals for evaluation. While Motorola (to no one’s surprise) won the competition, Dorothy and I believed that we shouldn’t have won. In particular, our arch-enemies at Sagem Morpho raised a compelling argument that it should be the chosen vendor.

Their argument? Here’s my summary: “Your RFP says that you want a Motorola AFIS. The states of Kansas (see page 6 of this PDF) and New Mexico (see this PDF) USED to have a Motorola AFIS…but replaced their systems with our MetaMorpho AFIS because it’s BETTER than the Motorola AFIS.”

But were Cogent, Motorola, NEC, and Sagem Morpho the only “big” players?

Did the Big 3 become the Big 5?

While the Big 3/Big 4 took a lot of the headlines, there were a number of other companies vying for attention. (I’ve talked about this before, but it’s worthwhile to review it again.)

Identix, while making some efforts in the AFIS market, concentrated on creating live scan fingerprinting machines, where it competed (sometimes in court) against companies such as Digital Biometrics and Bioscrypt.

The fingerprint companies started to compete against facial recognition companies, including Viisage and Visionics.

Oh, and there were also iris companies such as Iridian.

And there were other ways to identify people. Even before 9/11 mandated REAL ID (which we may get any year now), Polaroid was making great efforts to improve driver’s licenses to serve as a reliable form of identification.

In short, there were a bunch of small identity companies all over the place.

But in the course of a few short years, Dr. Joseph Atick (initially) and Robert LaPenta (subsequently) concentrated on acquiring and merging those companies into a single firm, L-1 Identity Solutions.

These multiple mergers resulted in former competitors Identix and Digital Biometrics, and former competitors Viisage and Visionics, becoming part of one big happy family. (A multinational big happy family when you count Bioscrypt.) Eventually this company offered fingerprint, face, iris, driver’s license, and passport solutions, something that none of the Big 3/Big 4 could claim (although Sagem Morpho had a facial recognition offering). And L-1 had federal contracts and state contracts that could match anything that the Big 3/Big 4 offered.

So while L-1 didn’t have a state AFIS contract like Cogent, Motorola, NEC, and Sagem Morpho did, you could argue that L-1 was important enough to be ranked with the big boys.

So for the sake of argument let’s assume that there was a Big 5, and L-1 Identity Solutions was part of it, along with the three big boys Motorola, NEC, and Safran (who had acquired Sagem and thus now owned Sagem Morpho), and the independent Cogent Systems. These five companies competed fiercly with each other (see West Virginia, above).

In a two-year period, everything would change.

The Big 3 after 2009

Hang on to your seats.

The Motorola RAZR was hugely popular…until it wasn’t. Eventually Motorola split into two companies and sold off others, including the “Printrak” Biometric Business Unit. By NextG50 – Own work, CC BY-SA 4.0, https://commons.wikimedia.org/w/index.php?curid=130206087

By 2009, Safran (resulting from the merger of Sagem and Snecma) was an international powerhouse in aerospace and defense and also had identity/biometric interests. Motorola, in the meantime, was no longer enjoying the success of its RAZR phone and was looking at trimming down (prior to its eventual, um, bifurcation). In response to these dynamics, Safran announced its intent to purchase Motorola’s Biometric Business Unit in October 2008, an effort that was finalized in April 2009. The Biometric Business Unit (adopting its former name Printrak) was acquired by Sagem Morpho and became MorphoTrak. On a personal level, Dorothy Bullard moved out of Proposals and I moved into Proposals, where I got to work with my new best friends that had previously slammed Motorola for losing the Kansas and New Mexico deals. (Seriously, Cindy and Ron are great folks.)

By 2011, Safran decided that it needed additional identity capabilities, so it acquired L-1 Identity Solutions and renamed the acquisition as MorphoTrust.

If you’re keeping notes, the Big 5 have now become the Big 3: 3M, Safran, and NEC (the one constant in all of this).

While there were subsequent changes (3M sold Cogent and other pieces to Gemalto, Safran sold all of Morpho to Advent International/Oberthur to form IDEMIA, and Gemalto was acquired by Thales), the Big 3 has remained constant over the last decade.

And that’s where we are today…pending future developments.

If Alphabet or Amazon reverse their current reluctance to market their biometric offerings to governments, the entire landscape could change again.

Or perhaps a new AI-fueled competitor could emerge.

The 1 Biometric Content Marketing Expert

This was written by John Bredehoft of Bredemarket.

If you work for the Big 3 or the Little 80+ and need marketing and writing services, the biometric content marketing expert can help you. There are several ways to get in touch:

Book a meeting with me at calendly.com/bredemarket. Be sure to fill out the information form so I can best help you.

Back on October 23, 2007, I used my then-active Twitter account to tweet about the #sandiegofire. The San Diego fire was arguably the first mass adoption of hashtags, building upon pioneering work by Stowe Boyd and Chris Messina and acted upon by Nate Ritter and others.

The tinyurl link directed followers to my post detailing how the aforementioned San Diego Fire was displacing sports teams, including the San Diego Chargers. (Yes, kids, the Chargers used to play in San Diego.)

So while I was there at the beginning of hashtags, I’m proudest of the post that I wrote a couple of months later, entitled “Hashtagging Challenges When Events Occur at Different Times in Different Locations.” It describes the challenges of talking about the Rose Parade when someone is viewing the beginning of the parade while someone else is viewing the end of the parade at the same time. (This post was cited on PBWorks long ago, referenced deep in a Stowe Boyd post, and cited elsewhere.)

Hashtag use in business

Of course, hashtags have changed a lot since 2007-2008. After some resistance, Twitter formally supported the use of hashtags, and Facebook and other services followed, leading to mass adoption beyond the Factory Joes of the world.

Ignoring personal applications for the moment, hashtags have proven helpful for business purposes, especially when a particular event is taking place. No, not a fire in a major American city, but a conference of some sort. Conferences of all types have rushed to adopt hashtags so that conference attendees will promote their conference attendance. The general rule is that the more techie the conference, the more likely the attendees will use the conference-promoted hashtag.

I held various social media responsibilities during my years at MorphoTrak and IDEMIA, some of which were directly connected to the company’s annual user conference, and some of which were connected to the company’s attendance at other events. Obviously we pulled out the stops for our own conferences, including adopting hashtags that coincided with the conference theme.

And then when the conference organizers adopt a hashtag, they fervently hope that people will actually USE the adopted hashtag. As I said before, this isn’t an issue for the technical conferences, but it can be an issue at the semi-technical conferences. (“Hey, everybody! Gather around the screen! Someone used the conference hashtag…oh wait a minute, that’s my burner account.”)

A pleasant surprise with exhibitor/speaker adoption of the #connectID hashtag

Well, I think that we’ve finally crossed a threshold in the biometric world, and hashtags are becoming more and more acceptable.

As I previously mentioned, I’m not attending next week’s connect:ID conference in Washington DC, but I’m obviously interested in the proceedings.

I was pleasantly surprised to see that nearly two dozen exhibitors and speakers were using the #connectID hashtag (or referenced via the hashtag) as of the Friday before the event, including Acuity Market Intelligence, Aware, BIO-key, Blink Identity, Clearview AI, HID Global, IDEMIA, Integrated Biometrics, iProov, Iris ID, Kantara, NEC and NEC NSS, Pangiam, Paravision, The Paypers, WCC, WorldReach Software/Entrust, and probably some others by the time you read this, as well as some others that I may have missed.

And the event hasn’t even started yet.

At least some of the companies will have the presence of mind to tweet DURING the event on Tuesday and Wednesday.

Will yours be one of them?

But company adoption is only half the battle

While encouraging to me, adoption of a hashtag by a conference’s organizers, exhibitors, and speakers is only the beginning.

The true test will take place when (if) the ATTENDEES at the conference also choose to adopt the conference hashtag.

According to Terrapin (handling the logistics of conference organization), more than 2,500 people are registered for the conference. While the majority of these people are attending the free exhibition, over 750 of them are designated as “conference delegates” who will attend the speaking sessions.

How many of these people will tweet or post about #connectID?