Yacht Rock Man is too immersed.

Tag Archives: finance

Underwriting the Ghost: Synthetic Borrowers Disappear Without Paying

When a lender receives a loan application, it endeavors to ensure that the applicant will pay the lender back.

But even with the proper controls, a certain percentage of loans go unpaid.

Especially if the applicant looks really good on paper, but isn’t…and doesn’t even exist because it’s a synthetic identity.

PYMNTS describes the threat from deepfake borrowers:

“Across the lending industry, a new category of fraud is emerging that combines deepfake video, cloned voices, synthetic identity creation, fabricated employment histories and AI-generated financial behavior into a single engineered persona. These synthetic borrowers are not merely fake identities in the traditional sense. They are algorithmically optimized consumers designed to survive onboarding checks, satisfy underwriting models and disappear once loans are funded.”

Disappearing borrowers is not a good thing.

Know your customer.

“Accept Without Posting” Issue Resolved…Even Though I Appeared To Be Very Evil

Here’s the resolution to the “Accept Without Posting” issue that I discussed on Saturday.

You’ll recall that I initiated a Zelle transfer to my account at “the blue bank,” but the blue bank “placed this transfer on hold so they can conduct further review.”

With no word on what the blue bank was reviewing. And the “blue bank” representative whom I spoke with on Saturday didn’t know either.

- I had already ruled out the simple explanations, such as either the sending Zelle account or the receiving Zelle account didn’t exist.

- I figured that perhaps my use of Zelle was the issue. The day before I sent the “on hold” transaction, I had sent another transaction. I figured that two transactions in two days tripped up some odd alert of possible account draining.

Neither of these turned out to be the issue.

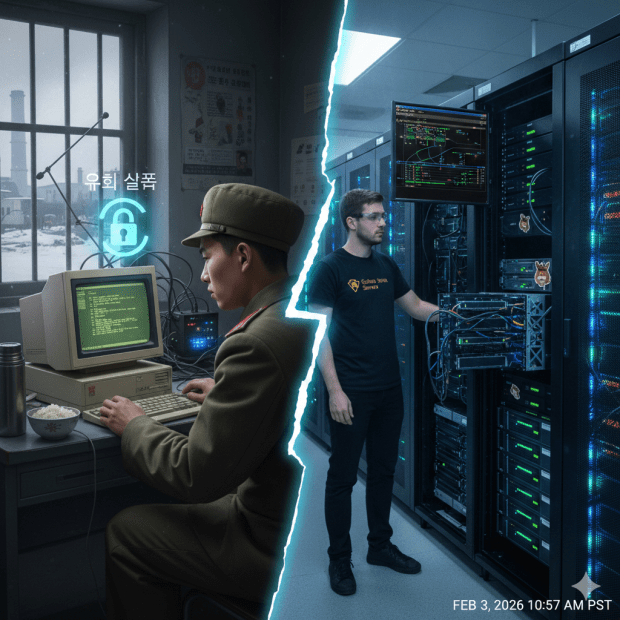

On Monday (just after I had rated the “blue bank” 5 out of 10 for its handling of the issue; coincidence, or no?) I received a call from someone at my local “blue bank” branch.

Turns out that the issue was the COMMENT that I attached to the Zelle transfer.

My comment referenced another individual. Without revealing this person’s personally identifiable information (PII), I will state that his first name begins with a K, his last name begins with a P, and he is a “Junior.” So because acronyms are wonderful, I referred to this person as “KP2” in the Zelle transfer field.

Which was an extremely evil thing to do, because that tripped up an anti-money laundering check.

Basically, anti-money laundering checks verify that a person isn’t transferring money for a sanctioned person.

And I didn’t trip up just ANY anti-money laundering check.

This one was bad.

Really bad.

How bad?

- Let’s look at ISO 3166 country codes. The alpha 2-digit country code for the Democratic People’s Republic of Korea (North Korea) is…KP. KP-02 is the specific administrative code for South Pyongan Province (Pyeonganbuk-do).

- And the Korean People’s Army includes a II Corps that is sometimes abbreviated as…KPA II Corps or KPA 2nd Corps.

Back to the call I received from my local “blue bank” branch. The representative didn’t go into all that, but just said that my comment about “KP2” looked like a reference to North Korea.

I burst out laughing.

I gave the “blue bank” representative the full name of K[REDACTED] P[REDACTED] Junior, explained that there were five “KP”s, and that I used numbers to tell them apart.

Ironically, both “KP2” and “KP4” are veterans. I wonder if they realize their initials associate them with this guy.

Anyway, my answer satisfied the banker, the hold was removed from the Zelle transfer, and I received the money within minutes.

And I know to be careful when using acronyms beginning with the letter “K” in financial transactions.

Verified Assets Only

This is a musical repurpose of my 2024 post “Know Your…Everyone.” I liked this Lyria effort better than the previous one on anti-money laundering. But just a little.

Accept Without Posting (I may be a fraudster, June 2026 edition)

Remember in March 2022 when I searched my (then) Twitter profile picture against TinEye and found 0 matches, indicating that I may be a fraudster because TinEye didn’t have a history on me?

Well, I found additional evidence of my supposed shady nature.

For purposes of this discussion, I will refer to the two banks in question as the “red” bank and the “blue” bank. (No political implications here.) I’ve previously referred to the blue bank as Wildebeest Bank, but today I’m sticking to the color scheme idea.

Both banks use Zelle to support instant transactions between member institutions, and I have Zelle-enabled accounts with both banks. For the record:

- I frequently perform immediate Zelle transfers from the blue bank to the red bank.

- On Wednesday, I successfully performed an immediate Zelle transfer from the red bank to the blue bank.

So on Thursday, I thought nothing of sending a second Zelle transfer from the red bank to the blue bank.

Until the red bank emailed me.

“The recipient bank [the blue bank] has placed this transfer on hold so they can conduct further review. Upon completion of the review, they will either complete your transfer or [the red bank] will contact you with more details. No further action is required from you at this time.”

Now why would a bank conduct further review? Three possible reasons.

- The recipient isn’t enrolled in Zelle. Not a problem here.

- The recipient bank is conducting a technical check. This shouldn’t be a problem here, since both Zelle accounts have been successfully used before.

- The recipient bank is conducting a fraud check. This, perhaps an anti-money laundering investigation, seems the most likely scenario, especially since this was launched one day after another transfer. Even though the second transfer is SMALLER than the first transfer, perhaps the one-day timeframe looks like someone is trying to drain the red bank account.

So this happened Thursday, and as of Saturday (two calendar days and one business day later) I hadn’t heard a thing.

So I called the blue bank, reached a helpful representative, and waited for her to research the issue. I heard her mutter over the phone:

“Accept without posting”

Then, a minute later:

“What does THAT mean?”

While I waited for her to officially talk to me again, I performed some online research and confirmed that “accept without posting” is another way of saying that the transaction is under review. Here’s what the Cleveland Federal Reserve says about FedNow, one bank transfer method:

“[T]he FedNow Service sends the payment information to the receiver’s financial institution and asks that bank to confirm that it intends to accept the payment message. It can accept, or reject, or accept without posting, which means some of the pre-checks of the transaction are pending or delayed.”

Then when the blue bank representative did speak to me, things got even more confusing as she said that there were notes from Monday involving “the green bank” that wasn’t even involved in the transaction. Wisconsin Travel Federation?

The representative didn’t have access to the group that put my Zelle transfer on hold, so for now I wait.

Technically it’s only been one business day.

The Bangladesh Identities Weren’t Synthetic Identities, But They Failed The “Somewhat You Why” Test

Andrew Austin at Sardine has written an eye-catching blog post that discusses a fraud ring exhibiting unusual patterns.

- Some fraudsters use synthetic identities to fool systems, but good systems can catch the synths.

- But other fraudsters use mules and other techniques that pass identity verification checks, because the people are REAL people.

Austin’s post discusses an example of the latter.

Sign-up patterns in Bangladesh

In this particular case (Example 3 of 3), a gig economy company had discovered a fraud ring operating out of Bangladesh, but the identities were those of real people. The investigator noticed something right off the bat:

“When we looked into it, something was off: all of the locations seemed to be clustered in a few small towns.”

But wait…it gets better.

“The fraudsters were going door-to-door and signing up anyone who was willing to share their information….

“Dozens of routes snaked through neighborhoods where new accounts were being created, each of them running from North to South and then back to their starting point on the next street over.”

It turns out that the fraudsters were going down each street, paying people to borrow their identities, and then moving on to the next street.

How identity factors (in the plural) identified the fraud

In Bredemarket’s view, this raised alarms surrounding two factors of identity verification and authentication.

- The first was geolocation. Once the identities were plotted, it seems strange that all of the identities lined up down each street and on to the next street.

- The second is what I call “somewhat you why.“ It’s reasonable to believe that if person A signs up for a service, their neighbors may sign up also. But it’s NOT reasonable to believe that people would sign up for the service in address order, moving from street to street. “No, Jim, 158 1st street can’t sign up for the service! 156 1st street hasn’t signed up yet!”

Now even if you don’t believe that “somewhat you why” is a real factor (Sardine prefers to talk about “device and behavior intelligence“), it’s clear that fraudsters were using the identities of real people to engage in a massive fraud scheme.

Look at the patterns, and you can discover from unusual ones.

And now a word from our sponsor

And if you’re wondering why I discuss SIX factors of identity verification and authentication (rather than five or three), check out my ebook “Proving Humanity: The Six Factors of Identity Verification and Authentication.”

Dry To The Bone

You’re not gonna hear this song about dry fingerprint ridges on Top 40 radio. But for a select few biometric product marketers, it highlights a critically important issue.

Why?

Because dry fingerprint ridges, while not a common worry among the general populace, ARE a concern among law enforcement, homeland security, financial institution, and other professionals who depend on high-quality friction ridge capture to solve crimes and identify people.

And these people desperately need products that accurately capture fingerprints in challenging conditions.

And the product vendors need to communicate their product benefits to potential vendors. (Whoops, I mean prospects.)

That’s where Bredemarket comes to save the day.

Not with music.

(Thankfully.)

Through Bredemarket, I work with you to develop the customer-focused, benefits-oriented words that move your prospects toward your fingerprint capture solution.

If you want prospects to buy your identity product, schedule a free meeting with the biometric product marketing expert.

And…I couldn’t resist one more.

Hype

The picture above and text below were authored by Google Gemini.

Get ready to maximize your reality because our quantum-powered, generative AI agent is autonomously deploying a CRISPR-edited, synthetic biopolymer directly into your 5G-connected smart-home fabricator to 3D-print a hyper-personalized, self-driving robotaxi—instantly minting the entire experience as a fractionalized, Web3 DeFi asset with a secure NFT deed that grants your holographic avatar VIP entry into a fully decentralized, spatial-computing metaverse!

Why Identity/Biometric Product Marketers Should Target Organizations Instead of Enterprises

Since I am not really a business-to-consumer guy, I tend to think of hungry people (target audiences) who number in the hundreds or thousands rather than millions. For example, if you want to sell your identity/biometric solutions to banks with total assets of over US$100 billion, there are only about 100 of them.

Marketing products in this environment requires a completely different mindset. Rather than hiring a Kardashian or Jenner as your influencer or spokesperson, you’d hire a Buffett. (If you could. You probably can’t, unless he owns the company.)

Therefore you need to concentrate on the players who make buying decisions, from the CxO level down to the users. That is the way to get your product into the enterprise.

But if enterprise penetration is your goal, you’re doomed to failure.

Why an enterprise-only strategy will fail

For example, enterprises usually don’t buy automated biometric identification systems. Government agencies do.

Believe me, I know. Many identity/biometric firms sell to the U.S. Department of Homeland Security, and their orders have been disrupted on and off since last October.

One acronym that I love to use is B2G—business-to-government. But I’ve learned the hard way that many people have never heard this acronym before. (Scan the job descriptions and spot the ones for marketing to government agencies that require “B2B” experience.)

So Bredemarket doesn’t seek clients that only sell to enterprises. I seek those that sell to organizations, both private and public.

If your identity/biometric or technology company markets products to organizations and you need strategic and tactical assistance, talk go Bredemarket.

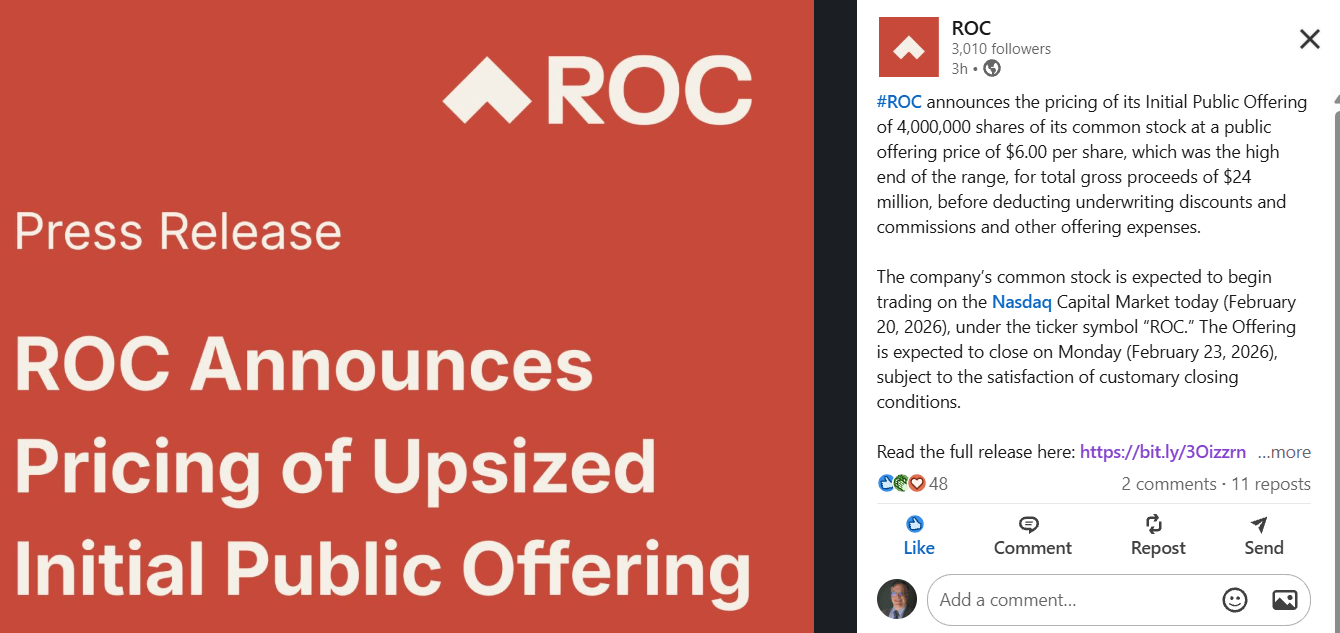

IPOs New and Old (ROC, Printrak)

Earlier this morning, ROC (formerly Rank One Computing) made an announcement:

“#ROC announces the pricing of its Initial Public Offering of 4,000,000 shares of its common stock at a public offering price of $6.00 per share, which was the high end of the range, for total gross proceeds of $24 million, before deducting underwriting discounts and commissions and other offering expenses.”

Six dollars a share doesn’t seem that impressive, but all companies have to start somewhere. If I recall correctly, Printrak’s price was in that range when it started public trading (under the then-trendy ticker “AFIS“) back in 1996.

ROC was able to secure its preferred ticker “ROC.” (Sorry Alcatraz.) And the stock is already trading; see Yahoo Finance for the latest movements.

Incidentally, I should state my views on the success of an IPO.

- Many think that if a stock is initially priced at $6.00, and the price zooms to $100 by the end of the day, the IPO is a success.

- I maintain that it’s a failure. A company wants to maximize its revenue, and if the stock was truly worth $100, it should have priced its IPO at $100 to realize maximum revenue.

- Conversely, if the stock opens at $6 and the end of day price is at about that level, then the IPO is a success because the company received the maximum revenue.

- Needless to say this doesn’t take employee holdings into account. But if the goal is to maximize IPO revenue, then a price that DOESN’T shoot up is a sign of success.