Here’s the resolution to the “Accept Without Posting” issue that I discussed on Saturday.

You’ll recall that I initiated a Zelle transfer to my account at “the blue bank,” but the blue bank “placed this transfer on hold so they can conduct further review.”

With no word on what the blue bank was reviewing. And the “blue bank” representative whom I spoke with on Saturday didn’t know either.

- I had already ruled out the simple explanations, such as either the sending Zelle account or the receiving Zelle account didn’t exist.

- I figured that perhaps my use of Zelle was the issue. The day before I sent the “on hold” transaction, I had sent another transaction. I figured that two transactions in two days tripped up some odd alert of possible account draining.

Neither of these turned out to be the issue.

On Monday (just after I had rated the “blue bank” 5 out of 10 for its handling of the issue; coincidence, or no?) I received a call from someone at my local “blue bank” branch.

Turns out that the issue was the COMMENT that I attached to the Zelle transfer.

My comment referenced another individual. Without revealing this person’s personally identifiable information (PII), I will state that his first name begins with a K, his last name begins with a P, and he is a “Junior.” So because acronyms are wonderful, I referred to this person as “KP2” in the Zelle transfer field.

Which was an extremely evil thing to do, because that tripped up an anti-money laundering check.

Basically, anti-money laundering checks verify that a person isn’t transferring money for a sanctioned person.

And I didn’t trip up just ANY anti-money laundering check.

This one was bad.

Really bad.

How bad?

- Let’s look at ISO 3166 country codes. The alpha 2-digit country code for the Democratic People’s Republic of Korea (North Korea) is…KP. KP-02 is the specific administrative code for South Pyongan Province (Pyeonganbuk-do).

- And the Korean People’s Army includes a II Corps that is sometimes abbreviated as…KPA II Corps or KPA 2nd Corps.

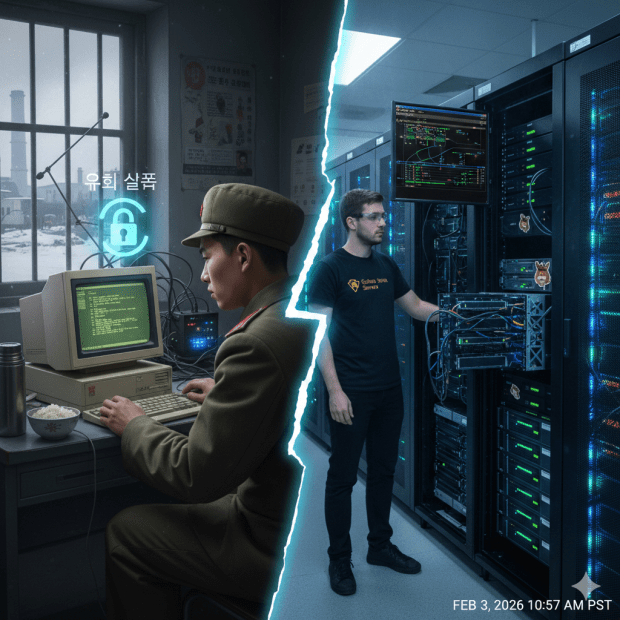

Back to the call I received from my local “blue bank” branch. The representative didn’t go into all that, but just said that my comment about “KP2” looked like a reference to North Korea.

I burst out laughing.

I gave the “blue bank” representative the full name of K[REDACTED] P[REDACTED] Junior, explained that there were five “KP”s, and that I used numbers to tell them apart.

Ironically, both “KP2” and “KP4” are veterans. I wonder if they realize their initials associate them with this guy.

Anyway, my answer satisfied the banker, the hold was removed from the Zelle transfer, and I received the money within minutes.

And I know to be careful when using acronyms beginning with the letter “K” in financial transactions.