The TL;DR…someone authenticates themselves after a delivery company request, but the actual delivery is made by a minor such as a younger brother or sister. As I noted, continuous authentication through the entire delivery process, rather than just at the beginning, nips this fraud in the bud.

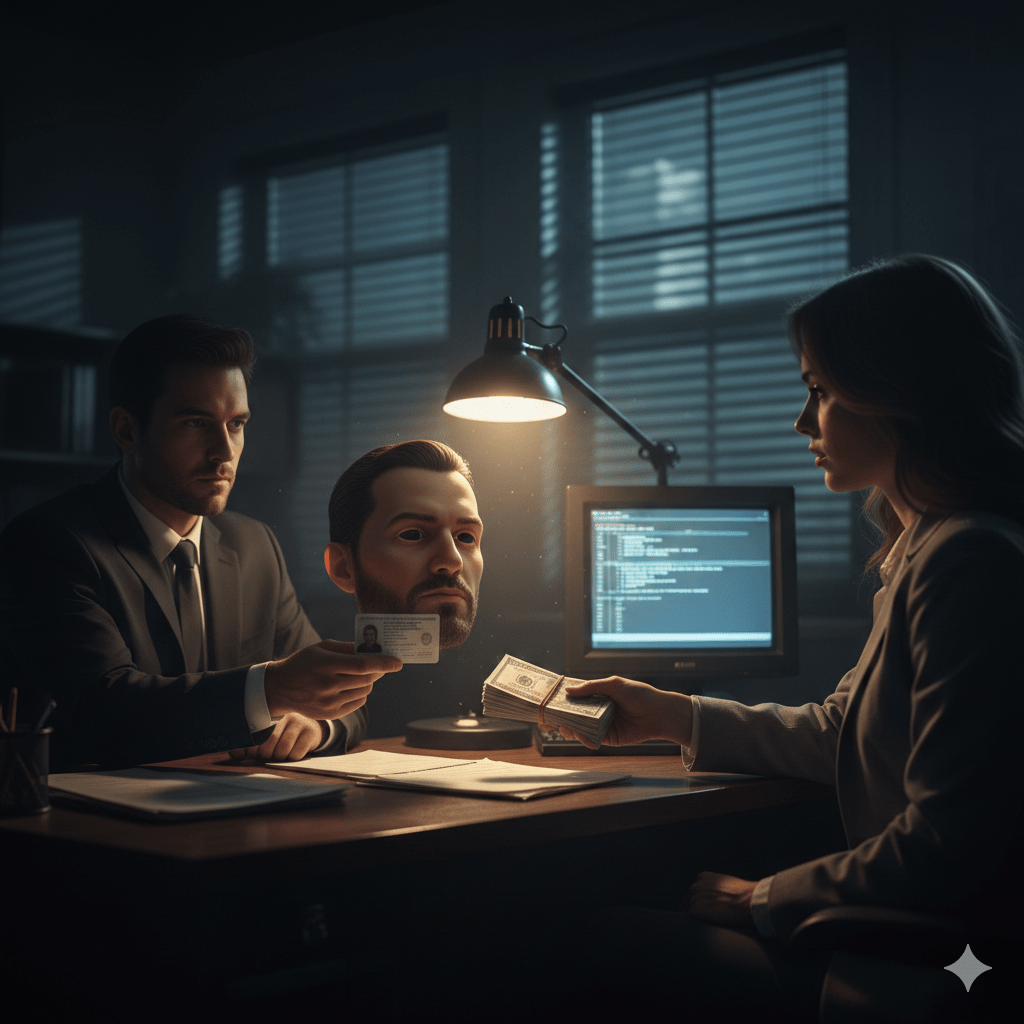

“A TransUnion report indicates that weak identity verification processes are leaving gig platforms, workers and consumers exposed to fraud and safety risks.

“The 2026 Gig Economy Worker Report reveals that one in four gig workers has rented or sold access to their accounts, enabling unverified individuals to perform services under their names.”

Of course ID renting is not limited to the gig economy.

Google Gemini.

The whole “money mule” effort is designed to obfuscate the original seller of goods by inserting an intermediary, with the intermediary’s rented identification the ID of record.

Whenever you let someone borrow your identity, you’re endangering everyone.

But there are ways to stop this. If your company offers such a solution, Bredemarket can help you publicize it. Talk to me.

And in case you’re wondering, yes I do my own work.

My 2024 offboarding post discussed the short-term aspects of how Bredemarket wraps up business with its clients. But it didn’t cover the long-term aspects.

What I didn’t say in 2024

You’ll recall my description of the end of a particular contract.

In 2023 I signed a contract with a client in which I would bill them at an hourly rate. This was a short-term contract, but it was subsequently renewed.

Recently the client chose not to renew the contract for another extended period.

But there’s one thing I didn’t say.

The client (whom I’ll call Client 1) failed to tell me that it wasn’t renewing my contract. In fact, in my last discussion with the client, I did not perceive that it wasn’t planning to renew.

Surprise! In fact, I learned of the non-renewal from a third party, not the client itself.

Of course, the client had every right to choose not to renew without advance notice.

But read on.

What happened in 2025

Contrast that with my relationship with two other existing clients, both of whom contacted me personally and let me know that they weren’t renewing my contract.

Both took the time to explain why they were not renewing. Nothing to do with my performance, but having to do with internal issues at each company (which I am not at liberty to discuss).

I went through the aforementioned data scrub process with both clients, and my obligation to both was done.

But read on.

Two little twists

Add these facts.

There was an interesting connection between Client 2 and Client 3. My primary employee contact at Client 2 was previously a consultant at Client 3 until they were let go (again, not because of performance, but because of internal issues).

And a little while later, my employee contact at Client 2 was let go from Client 2 themselves (again, internal issues).

The long term

Bredemarket completed its contractual obligations to all three firms: the one that let me go in 2024 (Client 1), and the two that let me go in 2025 (Client 2 and Client 3).

But what happens after that?

It depends.

If my employee contact at Client 3 requests help, or if I see something of interest to Client 3, I’ll be more than happy to help or share.

If my employee contact formerly of Client 2 requests help, or if I see something of interest to Client 2, I’ll be more than happy to help or share.

If I see something of interest that affects Client 2, I may or may not share.

If I see something of interest that affects Client 1, I probably won’t share…except to Client 1’s competitors.

“The country of Uzbekistan will lift visa requirements for U.S. travelers starting Jan. 1, 2026, offering Americans another country to visit visa-free. The police change, which was recently confirmed by the government, will allow U.S. citizens to enter visa-free for up to 30 days.”

Just don’t bring your surfboards. Uzbekistan is double-landlocked.

Imagine if Capitol Records employed age verification in 1963.

Some musicians reach superstardom in their early 20s, feeling tremendous pressure at a young age.

But sometimes they’re younger: when “Surfin’ U.S.A.” hit number 3 on Billboard and Cash Box, surf guitarists Carl Wilson and (soon to depart) David Marks were 16 and 14, respectively.

Of course, Capitol Records would face a bigger problem—Know Your Composer. Brian Wilson did not write the song alone.

Some of us authenticate ourselves to unlock our smartphones. Others authenticate to access confidential corporate information. A few authenticate to wield the power to annihilate the world.

The football and the biscuit

In the United States, the President (Commander-in-Chief) has a “biscuit.”

Google Gemini.

“The nuclear biscuit is a card with authentication codes that acts as the President’s personal key to unlocking America’s nuclear arsenal.

“The biscuit acts a lot like a two-factor authentication device or app. Its codes are updated regularly, and it works in connection with the nuclear football to verify the President’s identity. Without the biscuit, the President can’t order a nuclear strike, even if they have the football itself.”

“Something you have is quite an obvious one, you needed to have the actual Biscuit and the codes within.

“Something you know is when you opened the Biscuit. It had many codes printed on the cards and all were false apart from one. The President would have been told the position of the real code when he first took office. He would also be told each time the Biscuit was changed.

“For something you are, the phone line the President would need to contact has no number. It can only be contacted via a secure military phone. This phone would be handed to the President by one of his security team who would obviously not hand this phone to anyone but the President.”

Now you can argue that the phone line is not a TRUE something you are factor. A devious security team member could hand the phone to someone who SOUNDS like the President.

And there’s another complication.

Passing the football

Let’s say that a President is away from Washington. Say, at a school in Florida.

And all of a sudden attacks are launched in multiple U.S. cities.

What if an attack were launched in Florida, incapacitating the President, either temporarily of permanently?

In such an attack, the country and the world cannot afford to wait for hours for the football to be flown to wherever Richard Cheney is.

“Believing that the vice president should be a partner in national security policymaking, President Jimmy Carter assigned a football to Vice President Walter Mondale and this became the practice for future U.S. administrations.”

Outside the U.S. Russia has a similar system called the “Cheget,” and other nuclear countries presumably have similar procedures to authenticate the persons or persons authorized to launch nuclear weapons.

Your football and biscuit

If you are an identity vendor or customer, you may have your own authentication and authorization procedures. While a breach of your procedures won’t result in the annihilation of civilization, it could create its own damage.

Do you need help describing the security of your identity solution?

Apparently Ontario Travel Blog is ripping off Bredemarket’s posts, including my December 8 post “‘Tis the Season to Be Scammy.“

Ontario Travel Blog’s version tries to cover its tracks by changing key words in its verison of the post, leading to hilarious results.

“However earlier than you reply to that mysterious “secret Santa” and ship that reward (or these reward playing cards) TODAY to obtain a highly-valued reward in return…know your corporation.”

“Welcome to [Your Blog Name]! Your privacy is important to us. This Privacy Policy explains how we collect, use, and protect your information when you visit our website.”

Masha Borak of Biometric Update is writing about FaceKom again.

I discussed Borak’s previous article on FaceKom, which noted the alleged ties between FaceKom and the Hungarian government. The whole thing is a classic example of BENEFICIAL ownership, in which someone who is not the legal owner of a company may still benefit from it.

Borak returned to the theme in the current post:

“FaceKom, the identity verification company used by the Hungarian national digital identity program, has been acquired by major local IT and telecom group, 4iG Informatikai (4iG IT). The deal is now attracting attention among media outlets and political watchers due to the companies’ relationship with Prime Minister Viktor Orbán….

“Recent 4iG’s purchases, however, have been raising questions over the company’s reported links to the Hungarian government, which has been accused by critics of enriching political allies, family, and loyalists through state resources and public contracts.”

“4iG chairman and majority investor Gellért Jászai is known for his ties to Orbán and was invited as part of his entourage to Donald Trump’s Mar-a-Lago resort after the 2024 U.S. presidential election.”

“[FaceKom’s] previous owner is Equilor Fund Management, owned by the Central European Opportunity Private Equity Fund (CEOM)….While CEOM has no direct links with Orbán, local media investigations have discovered links with companies owned by the Prime Minister’s son-in-law, István Tiborcz.”

Mere links do not necessarily indicate illegal activity, and Hungarian law may differ from laws in other countries, but FaceKom is being watched.

I’m jumping ahead in the year-end post ridiculousness to cite Bredemarket’s two most notable accomplishments this year. Not to detract from my other accomplishments this year, but these two were biggies.

The second was my go-to-market effort for a Bredemarket client in September, which I discussed (without mentioning my participation) here. And there’s a video for that effort also.

Recent go-to-market.

I’ve accomplished many other things this year: client analyses, blog posts (both individually and in series), consultations, presentations, press releases, proposals, requirements documents, sales playbooks, and many more.

And I still have three more weeks to accomplish things.

During this shopping season, you will be offered incredible deals if you act NOW.

But before you respond to that mysterious “secret Santa” and send that gift (or those gift cards) TODAY to receive a highly-valued gift in return…know your business.